© The Financial Times Ltd 2016

FT and 'Financial Times' are trademarks of The Financial Times Ltd.

The Financial Times and its journalism are subject to a self-regulation regime under the FT Editorial Code of Practice.

June 16, 2015 12:17 pm

It was called the “blood oath”. The management team of Sandy Weill, an architect of the modern Citigroup and mentor to Jamie Dimon, had to commit not to sell any shares until they left.

In their decades as partnerships, Goldman Sachs and Morgan Stanley bankers had no need to open their veins. Holding equity until retirement was a binding legal restraint.

But that practice is not universal on Wall Street. A Financial Times analysis of insider selling at the six biggest US banks since the 2008 crisis shows that many of the current crop of executives have offloaded millions of dollars worth of stock each year.

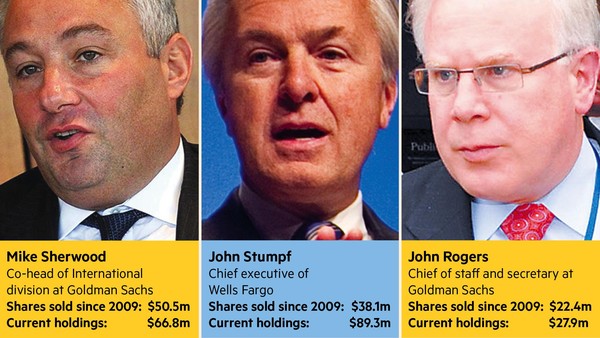

Interactive: Who sold

Compare the stock holdings of bank executives who have chosen to either cash out or keep stock as ‘skin in the game’

Some have done so beneath “book value”, a measure of how much of a company would be left for shareholders if it were liquidated. Companies trading at this level are either undervalued by the market or overstating the value of their assets.

The top executive for selling among the six largest US banks is Mike Sherwood, the London-based co-head of Goldman Sachs’ international division, who has offloaded more than $50m worth.

Sales since 2009 by executives at Bank of America, Citi, Goldman, JPMorgan Chase, Morgan Stanley and Wells Fargo were analysed using data from S&P Capital IQ, Bloomberg and regulatory filings.

Mr Sherwood is the clear leader over the timeframe, selling more than twice as much as his boss Lloyd Blankfein.

Known in his early days in the City of London in the late 1980s for his big pay cheques, he is now seen as an outside contender to succeed Mr Blankfein, and prefers the nickname “Woody”. As a result of banker pay rules in the UK, Mr Sherwood receives a larger proportion of his package in stock instead of cash than other Goldman executives.

The second-biggest seller was John Stumpf, chief executive of Wells Fargo, who has sold $38.1m of stock in his bank. While their roots are a long way from the Wall Street elite, Mr Stumpf and his colleagues at the San Francisco-based bank have cashed in more shares than most rivals.

Mr Stumpf’s second place — and the high ranking of his colleagues — could partly be a result of the relative outperformance of Wells Fargo’s stock in the past few years. But the stock performance does not account for the gulf between him and most other chief executives, some of whom make a point of selling nothing.

“Sales of shares by our executives were for personal reasons,” said the bank in a statement. “Our executive officers’ stock holdings continue to meet or exceed those required by Wells Fargo’s robust stock ownership policy for executive officers.”

To be sure, the previous generation of bankers were not all long-term holders. Ken Lewis and Dick Fuld sold tens of millions of dollars of stock in BofA and Lehman Brothers respectively in the run-up to the crisis. In the past and present, there have often been individual reasons to seek “liquidity”, notably divorce.

Today’s senior executives say they are caught between institutional investors who want them to hold the bulk of their wealth in the company as “skin in the game” and their financial advisers, and sometimes spouses, who urge them to diversify in case of disaster.

Many bankers are scarred by the demise of Lehman Brothers, Bear Stearns and Merrill Lynch, where employees who had kept their income in stock lost the majority of their wealth.

However, Lucian Bebchuk, director of the corporate governance programme at Harvard Law School and a former adviser to the US government’s “pay tsar”, argued there should be tighter restrictions on the amount of annual selling by executives.

“When bank executives have substantial freedom to unload equity incentives given to them as part of their compensation, and when executives can be expected to make significant use of their freedom to unload such equity incentives, the executives’ pay arrangements produce distorted incentives to engage in excessive risk-taking,” he said.

“Providing bank executives with desirable risk-taking incentives requires precluding them, as long as they lead their bank, from unloading a significant fraction of their holdings in any given year.”

Anne Simpson, senior portfolio manager and head of corporate governance at Calpers, the California pension fund, said: “We do prefer retention of shares, even post-retirement, to help with that long-term alignment of interest.”

We do prefer retention of shares, even post-retirement, to help with that long-term alignment of interest

- Anne Simpson, Calpers

The chief executive of a top-five bank said he would never sell below book value as it showed a lack of faith in the company. He said his colleagues should not be obliged to follow his example but he “felt sorry” for those who had sold and missed out on a subsequent rally.

That list includes the heads of investment banking at three of Wall Street’s leading institutions. In total, Colm Kelleher of Morgan Stanley has sold $6.9m of stock, Jamie Forese of Citi has sold $3.5m and Daniel Pinto of JPMorgan has sold $21.6m since 2009.

Mr Kelleher’s decision to sell meant he missed out on much bigger paper profits as Morgan Stanley’s stock quadrupled from its 2008 nadir.

Mr Forese also left money on the table, although Citi still remains below book value.

By contrast, only a small fraction of Mr Pinto’s selling occurred when the shares traded below book — and they did so only barely — but he is a relatively heavy seller of JPMorgan stock overall, placing him fifth on the table of executive sellers over the period. The analysis excludes non-executive directors and executives who have retired.

The banks all have similar restrictions in place, which often include keeping at least 50 per cent of the stock awarded. Some recipients choose to go closer to that line than others.

Mr Dimon, hewing to the ways of his former mentor Mr Weill, has “not sold a single share of JPMorgan Chase common stock”, the company said in its latest annual meeting filing to shareholders.

$473.6m

Total value of Lloyd Blankfein’s shareholding in Goldman Sachs

James Gorman at Morgan Stanley is a net acquirer of stock in his bank, spending $2.1m in August 2011 at a time when there were doubts about its long-term survival. It proved a good trade: the shares have almost doubled from $20.62 to $39.54.

Mike Corbat, Citigroup chief, and Brian Moynihan, head of Bank of America, have also not sold, at least while they have been chief executives. The Securities and Exchange Commission only requires top executives to disclose their trading and it is possible that they and others had sold earlier in their long careers at the banks.

Citi and BofA are poorly represented at the top of the table, which may indicate executives are holding shares because of confidence in the future. But it is also influenced by the relatively weak performance over several years which has discouraged selling and reduced their net worth.

Mr Moynihan’s total holdings of BofA stock are worth $13.6m while Mr Corbat has $22.5m of Citi stock. That is eclipsed many times over by the richest bank chiefs — Mr Blankfein has $477m of Goldman stock; Mr Dimon has $418m of JPMorgan stock — and even by many other lower-ranked executives at the top banks. The Citi chief executive is 18th on the list while the BofA chief is 33rd.

Copyright The Financial Times Limited 2017. You may share using our article tools.

Please don't cut articles from FT.com and redistribute by email or post to the web.

- Jeff Bezos' space company, Blue Origin, to bring hundreds of jobs to Alabama

- New study casts doubt on the benefit of Seattle's $15 minimum wage

- Avis to manage Waymo's self-driving cars

- Arconic halts sale of Grenfell Tower cladding panels for high rises

- Hedge fund star Dan Loeb bets $3.5 billion on Nestle

TOOLS & SERVICES

Multimedia

Tools

- Portfolio

- Topics

- FT Lexicon

- FT clippings

- Currency converter

- MBA rankings

- Newslines

- Today's newspaper

- FT press cuttings

- FT ePaper

- Ebooks

- Economic calendar

Services

Quick links

- FT Live

- How to spend it

- The 125

- FT Property Listings

- Social Media hub

- The Banker

- The Banker Database

- Global Risk Regulator

- fDi Intelligence

- fDi Markets

- fDi Benchmark

- Professional Wealth Management

- This is Africa

- Investors Chronicle

- MandateWire

- FTChinese.com

- Pensions Expert

- New York Institute of Finance

- ExecSense

- FT Confidential Research